The economy is highly integrated into international value chains, making it vulnerable to major foreign trade losses, especially in the automotive sector.

Political situation

Minority government supported by the communist party

The current coalition government between the populist party “ANO 2011” (“Yes 2011”) and the leftist Czech Social Democratic Party (CSSD) is still lacking a majority with only 93 seats in the 200-member parliament. Therefore, it repeatedly had to rely on the support of the pro-Russian Czech Communist Party, which since then has an informal role in the government – for the first time since 1989.

Pressure on Prime Minister Andrej Babis from the ANO 2011 has recently decreased as public prosecutors decided to drop criminal charges against him, related to an alleged misuse of EUR 2 million in European Union funds. While there have been regular demonstrations demanding his resignation, he and his party still enjoy wide popular support.

Economic situation

External headwinds impact economic growth

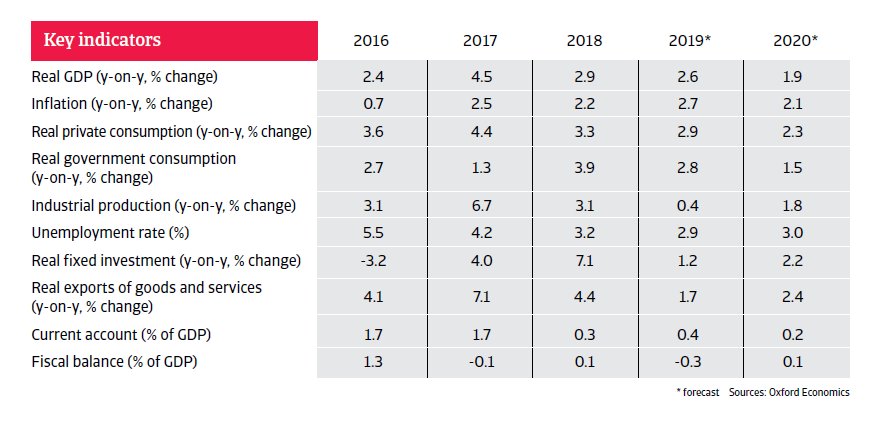

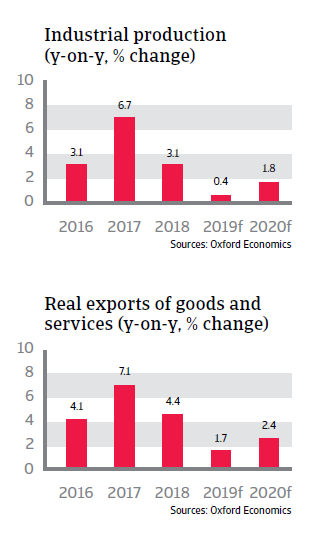

After robust growth rates in the last couple of years, when exports were supported by the country´s improved international competitiveness, GDP growth is expected to increase at a slower pace in 2019 and 2020. Both domestic and eurozone demand have decreased (e.g. lower demand from the German automotive industry). Industrial production and export growth are forecast to slip below 3% in 2019 and 2020.

Labour shortages are increasingly an issue, with many firms finding it difficult to fill vacancies, and rising labour costs have impacted the margins of businesses. Rising inflation, due to surging wages and increasing house prices, led to several benchmark interest rate increases by the Central Bank to 2.0% in August 2019. The tighter monetary policy has a dampening effect on investments and private consumption growth.

Government finances are solid due to income growth and increased tax compliance. At 30% of GDP government debt is low compared to other countries in the region, and is expected to decrease further. The good state of public finances means that the Czech Republic should have no troubles adhering to the adoption criteria of the euro. However, entering the eurozone still remains a controversial issue in Czech politics, with public opinion against it. Therefore, a eurozone entry in the coming years seems unlikely.

High export-dependency a potential risk factor

At more than 75%, the Czech Republic’s export-to-GDP ratio is one of the highest in the EU. And due to foreign investment, the Czech economy is highly integrated into international value chains. This makes the country vulnerable to major foreign trade losses. The main risks are a rapid exchange rate appreciation hurting international competitiveness and sharp declines in external demand, e.g. triggered by increased political uncertainty (Brexit), further escalation of international trade disputes and a major slowdown in the Eurozone.

Czech exports are also vulnerable to adverse developments in the automotive sector. The current challenges in the industry (decreasing sales and profits, shift to more e-mobility away from combustion engines and potential US tariffs on car and car part imports from the EU) pose a major downside risk.

Relaterte dokumenter

4.67MB PDF