Despite low confidence and modest 1.2% GDP growth in 2019, the construction sector performed quite well in terms of volume, and value added increased more than 2%.

Market Monitor Construction Belgium overview

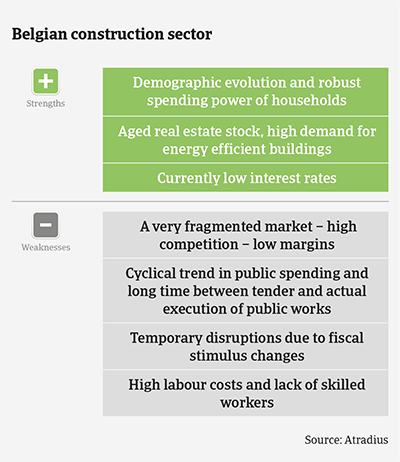

Persistent low interest rates were the main driver of growth, stimulating investors to place money in residential and commercial real estate (mainly offices and logistics buildings). Prices increased in almost all real estate segments.

However, downside risks for construction performance in 2020 and beyond have increased. Belgium´s economic outlook remains subdued, with annual growth rates of 1.1% expected in 2020 and 2021 (the construction sector usually follows economic cycles with some delay). Additionally, in some regions there is a potential risk of the market overheating due to an oversupply of new (overpriced) buildings.

A more difficult year ahead

After the May 2019 general elections forming a new government has proved to be difficult, and the country is still governed by a caretaker administration. For the time being, the investment policies of the incumbent or any new government (affecting public construction and infrastructure) remain uncertain. This also applies to future fiscal and tax policies (potential incentives for residential and commercial construction). The increased public construction activity starting ahead of the May 2019 federal and regional elections has meanwhile abated.

Residential construction activity is sustained by low interest rates and high demand for energy efficient buildings. However, there is some uncertainty over the impact of the phase out of the “woonbonus” (a tax reduction for mortgage loans that stimulated households to buy their own homes) in the region of Flanders since January 2020. Much depends on how interest rates will evolve. Commercial construction is impacted by the sluggish performance of the Belgian economy, hampering larger business investment.

Despite elevated working volumes seen in 2019, margins of construction businesses remained very low due to high competition, especially in the public tendering business, and the margin situation does not seem to be improving in 2020. The bargaining power of (smaller) subcontractors and suppliers has decreased. High labour costs remain an issue, and the lack of skilled staff often limits construction companies’ ability to provide higher volumes.

At the same time, delays in the start-up of projects remain common. This reduces the time to prepare work since contractors need to respond swiftly once an order has been placed. In the private sector customers tend to split building projects into parts, which increases tendering costs. The final settlement of projects can take a very long time as well.

Market Monitor Construction Belgium 2020 sector growth

Ongoing market consolidation and new working activities

The Belgian construction sector remains highly fragmented; however, consolidation in the market is ongoing. We expect that in the coming two years one in four general contractors will adapt different/new working activities to improve efficiency and productivity. Such businesses increasingly try to turn to more project development/coordination and renovation activities. Additionally the focus is increasingly on energy efficiency, sustainability, new techniques, circular construction and Building Information Modeling (BIM).

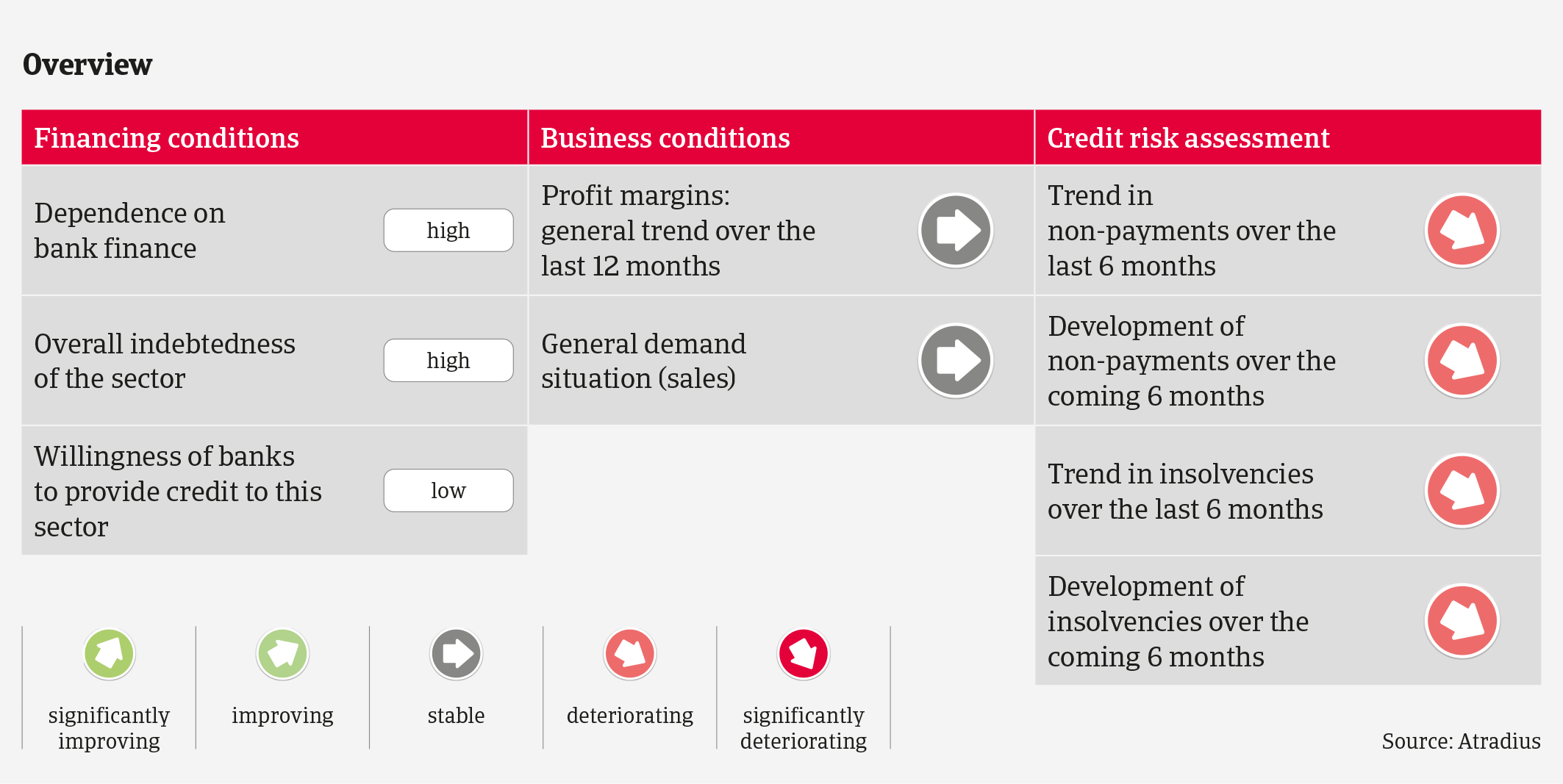

Such a shift in business activity requires sufficient financial resources, but in many cases we notice that banks are reluctant to finance those projects. This drives construction companies to look for alternative ways of financing. Smaller companies unable to finance and/or to cope with the shift to new fields of activity/new technologies will probably lose their competitive edge (especially against larger players) and experience more troubles in the future.

A bad payment experience over the past two years

In 2019, many construction companies were still confronted with defaulting payers (high DSO), and few Belgian companies are paid in advance. In general, payment terms tend to be long in the sector, i.e. “60 days end of month” is very common.

Payment experience has been bad over the past two years, and the number of non-payment notifications in the sector was high in 2019, with no major improvement expected in 2020. Construction insolvencies increased more than 8% year-on-year between January and November 2019, higher than the average growth rate of businesses failures overall during this period. In 2020, construction insolvencies are expected to increase further, although at a lower level (up 2%-3%).

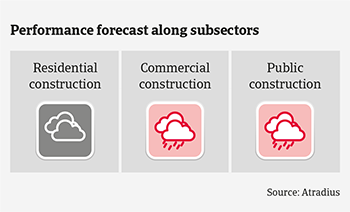

Our current underwriting stance is neutral for the residential construction segment, but rather restrictive for commercial and public construction. In order to sustain our risk appetite, it is necessary to identify the most affected companies/subsectors and to contact buyers for up-to-date financial information and performance outlooks. We examine the flexibility of companies (fixed cost structure), and whether they are able to build a buffer against potential economic downturns.

Market Monitor Construction Belgium 2020 strengths & weaknesses

Market Monitor Construction Belgium 2020 performance forecast

Relaterte dokumenter

1.42MB PDF